The following entities do not file or pay franchise tax:

- sole proprietorships (except for single member LLCs);

- general partnerships when direct ownership is composed entirely of natural persons (except for limited liability partnerships);

- entities exempt under Tax Code Chapter 171, Subchapter B;

- certain unincorporated passive entities;

- certain grantor trusts, estates of natural persons and escrows;

How much is franchise tax in Texas?

In Texas, businesses with $1.18 million to $10 million in annual receipts pay a franchise tax of 0.375%. Businesses with receipts less than $1.18 million pay no franchise tax. The maximum ...

Who has to pay Texas franchise tax?

Franchise tax taxes all the businesses involved in the process from the manufacturer to the end distributor. It can be considered a tax for the privilege of doing business in Texas. Who Needs to File for Texas Franchise Tax? The short answer is everyone who has nexus in Texas has to file & pay Texas franchise tax.

How to file Texas franchise annual report?

To successfully file your Texas Franchise Tax Report, you’ll need to complete these steps:

- Determine your due date and filing fees.

- Complete the report online OR download a paper form.

- Submit your report to the Texas Comptroller of Public Accounts.

What is the Texas franchise law?

Texas has not enacted franchise specific laws and is not a franchise registration state. However, Texas has enacted Business Opportunity Laws and, before offering or selling a franchise in Texas, you must first file a one-time Business Opportunity Exemption Notice with the Texas Secretary of State.

What is considered revenue for Texas franchise tax?

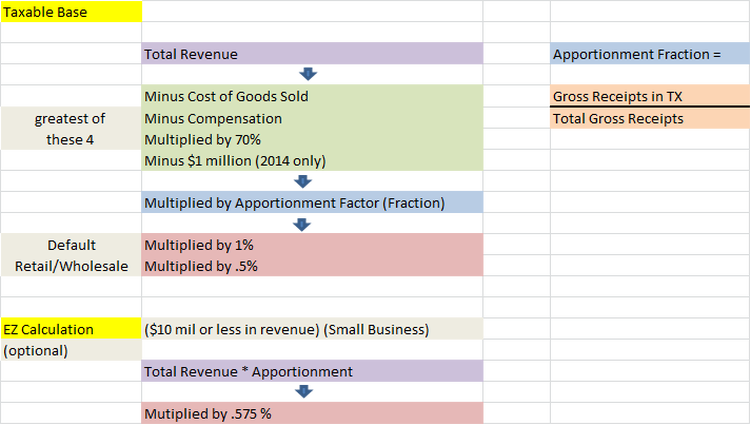

The Texas Franchise Tax is calculated on a company's margin for all entities with revenues above $1,230,000. The margin's threshold is subject to change each year.

What is exempt from Texas sales tax?

While the Texas sales tax of 6.25% applies to most transactions, there are certain items that may be exempt from taxation. This page discusses various sales tax exemptions in Texas....Other tax-exempt items in Texas.CategoryExemption StatusFood and MealsGrocery FoodEXEMPTLeases and RentalsMotor VehiclesEXEMPT *19 more rows

What is a disregarded entity for Texas franchise tax?

Disregarded Entities Therefore, partnerships, LLCs and other entities that are disregarded for federal income tax purposes are considered separate legal entities for franchise tax reporting purposes. The separate entity is responsible for filing its own franchise tax report unless it is a member of a combined group.

What is the Texas franchise tax threshold for 2022?

$1,230,000For the 2022 report year, a passive entity as defined in Texas Tax Code Section 171.0003; an entity that has total annualized revenue less than or equal to the no tax due threshold of $1,230,000; an entity that has zero Texas gross receipts; an entity that is a Real Estate Investment Trust (REIT) meeting the ...

Who is exempt from Texas franchise tax?

A nonprofit corporation organized under the Development Corporation Act of 1979 (Article 5190.6, Vernon's Texas Civil Statutes) is exempt from franchise and sales taxes. The sales tax exemption does not apply to the purchase of an item that is a project or part of a project that the corporation leases, sells or lends.

What qualifies you to be exempt from taxes?

To be exempt from withholding, both of the following must be true: You owed no federal income tax in the prior tax year, and. You expect to owe no federal income tax in the current tax year.

Who is subject to Texas franchise tax?

Texas Tax Code Section 171.001 imposes franchise tax on each taxable entity that is formed in or doing business in this state. All taxable entities must file completed franchise tax and information reports each year.

Are LLCs subject to Texas franchise tax?

Therefore, each taxable entity that is organized in Texas or doing business in Texas is subject to franchise tax, even if it is treated as a disregarded entity for federal income tax purposes and is required to file a franchise tax report.

What is a disregarded entity?

A disregarded entity is a business entity that (1) has a single owner, (2) is not organized as a corporation, and (3) has not elected to be taxed as a separate entity for federal tax purposes. The owner of a disregarded entity reports the income of the disregarded entity on the owner's return.

Do single member LLCs pay franchise tax in Texas?

The following entities do not file or pay franchise tax: sole proprietorships (except for single member LLCs);

Can you write off franchise tax?

While these "privilege taxes" may not make business owners happy, the good news is that the IRS allows you to deduct state franchise taxes when you prepare your federal tax return.

How is franchise tax calculated?

Divide your total gross assets by your total issued shares carrying to 6 decimal places. ... Multiply the assumed par by the number of authorized shares having a par value of less than the assumed par. ... Multiply the number of authorized shares with a par value greater than the assumed par by their respective par value.More items...

What is taxable in Texas sales tax?

Texas imposes a 6.25 percent state sales and use tax on all retail sales, leases and rentals of most goods, as well as taxable services.

What is a non taxable item?

Some items are exempt from sales and use tax, including: Sales of certain food products for human consumption (many groceries) Sales to the U.S. Government. Sales of prescription medicine and certain medical devices. Sales of items paid for with food stamps.

How do I check my Texas tax exempt status?

Questions about state tax-exempt status? Review the comptroller's FAQs or contact the comptroller's Exempt Organizations Section by phone at (800) 531-5441 or (512) 463-4600 or by email.

What does tax exempt mean for a business?

Organizations organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, educational, or other specified purposes and that meet certain other requirements are tax exempt under Internal Revenue Code Section 501(c)(3).

What is the TTC section 171.1011?

TTC Sections 171.1011 (r) and (s) allow an exclusion from total revenue for revenue received from oil or gas produced by a low-producing well (described in the next FAQ) during the Comptroller-certified dates when the monthly average closing price of West Texas Intermediate crude oil is below $40 per barrel or the average closing price of gas is below $5 per MMBtu, as recorded on the New York Mercantile Exchange (NYMEX).

Is bad debt expensed for federal income tax purposes?

Bad debt expensed for federal income tax purposes that corresponds to items of gross receipts included in total revenue for the current reporting period or a past reporting period may be excluded from total revenue. The principal repayment of a loan is not included in total revenue and therefore cannot be excluded from total revenue as a bad debt.

Can uncompensated care be subtracted from total revenue?

Yes, the costs of uncompensated care that have been excluded from total revenue may not be subtracted as cost of goods sold or compensation. If a health care provider excludes from total revenue payments received under the Medicaid, Medicare and other programs specified in Texas Tax Code (TTC) §171.1011 ...

Is franchise expense reimbursement included in total revenue?

Therefore, for franchise tax reporting purposes, the expense reimbursements are included in total revenue.

Can a taxable entity exclude from total revenue?

Under TTC 171.1011 (e) a taxable entity can only exclude from total revenue the taxable entity's share of net income of the passive entity if the margin of a taxable entity generated the net income of the passive entity. Therefore, a taxable entity that owns an interest in a passive entity may only exclude from total revenue, to the extent included:

What is franchise tax in Texas?

What is the Texas Franchise Tax? The Texas Franchise Tax is levied annually by the Texas Comptroller on all taxable entities doing business in the state. The tax is based upon the entity’s margin, and can be calculated in a number of different ways.

How to file a franchise tax report in Texas?

How to File. There are three ways to file the Texas Franchise Tax Report: No Tax Due. EZ Computation. Long Form. If your business falls under the $1,110,000 revenue limit, then you don’t owe any franchise tax. If you are above the limit, you can choose to fill out and file the EZ Computation form or to take the time to fill out the Long Form.

How is Total Revenue Calculated?

Total revenue is calculated by taking revenue amounts reported for federal income tax and subtracting statutory exclusions.

How many types of franchise tax extensions are there?

There are four different types of Franchise Tax Extensions, depending upon your situation.

Does compensation include 1099?

Compensation does not include 1099 labor or payroll taxes paid by the employer.

What is the purpose of exclusion in Titan Transportation v. Combs?

Combs, the Austin Third Court of Appeals held the taxpayer was entitled to exclude from total revenue payments made to its subcontractors that were providing services for its customers under Texas Tax Code (TTC) § 171.1011(g)(3), which provides: “A taxable entity shall exclude from its total revenue…only the following flow-through funds that are mandated by contract to be distributed to other entities...”2 The Third Court of Appeals explained that the term “other entities” means someone other than the taxpayer and further clarified: “[the] purpose of the (g)(3) exclusion is to prevent double taxation of funds that are not truly gain or income to the taxpayer, and this purpose is satisfied regardless of whether the mandate is contained in a contract with a customer or with a subcontractor.”3

When did Texas release COGS?

On June 30, 2016, the Texas Comptroller of Public Accounts (Comptroller) released a memorandum announcing a revised franchise tax policy on exclusions and the cost of goods sold (COGS) deduction.1 The revised policy allows for the exclusion of certain subcontracting payments that qualify as flow-through funds and expands the interpretation of furnished labor or materials for a project for purposes of the COGS deduction.

What is the COGS deduction in Combs v. Newpark?

Newpark Resources Inc., the Third Court of Appeals found the taxpayer’s activities of removal and disposal of waste materials from oil and gas well drilling sites qualified for a COGS deduction under TTC § 171.1012(i).4 TTC § 171.1012(i) provides: “A taxable entity furnishing labor or materials to a project for the construction, improvement, remodeling, repair, or industrial maintenance of real property is considered to be an owner of that labor or materials and may include the costs…in the computation of cost of goods sold.”

What is the exemption for franchise tax in Texas?

One of the most important exemptions for the Texas franchise tax is the exempt passive entity. Exempt passive entities will be required to file annual information statements to verify that the passive entity qualifications are met, but they will owe zero tax.

What is a taxable entity in Texas?

In addition, taxable entities include not only corporations and LLCs, but generally any entity with limited liability protection. Also introduced for the first time in Texas is the idea of unitary filing, something very alien to Texans. The only things that did not change are the due date of the tax, May 15 of each year, and the tax’s accounting period rules.

How is total revenue determined in Texas?

Total revenue is determined by extracting revenue from specific lines on the federal income tax forms (TX Tax Code §171.1011 (c) (1) (A)). Next, total revenue is reduced by applicable exclusions per Texas law. Exclusions tend to be based on industry, such as medical, legal, staff leasing services, and management companies (TX Tax Code §171.1011). Other exclusions include bad debt, income attributable to a disregarded entity, and net distributive income from partnerships and flowthrough partnerships (TX Tax Code §171.1011 (c) (1) (B)).

When to use tiered partnership?

Practice tip: The tiered partnership election should be used when the taxable entity is using the compensation deduction. Because some of the owners are other taxable entities, the lower-tier entity is not able to use the full compensation deduction through net distributive income. By making the election, the total tax paid by the lower- and upper-tier entities decreases. In addition, the upper-tier entities may elect to use either the deduction method or the E-Z method, even if the lower-tier entity does not use the same method, which could increase the tax savings even more. This is premised on the notion that the election need be available only at the lower level and not necessarily elected by the lower-level entity.

How to gain passive entity status?

Practice tip: For businesses selling real estate, one strategic plan is to form the entity as a partnership in order to gain passive entity status. Real estate entities should be passive entities as long as the sale of real estate results in a capital gain. Note that entities receiving real estate rental income should also be partnerships in case the real estate is sold for a capital gain. If a rental property is sold, it should be sold in the beginning of the year in order for the rental income to not be more than 90% of the total passive income for the tax year.

What is a state tax movement?

A current movement in state taxation is the introduction of a gross receipts or modified gross receipts tax in place of a net income tax. For example, Ohio, Kentucky, and New Jersey have all enacted some form of gross receipts tax in this decade. By joining this select crowd, Texas modified its old franchise tax, which was based on the capital or earned surplus of corporations and limited liability companies (LLCs) conducting business in Texas.

Can you deduct interest expense on a Texas COGS?

The rules also allow for a few small exceptions to the general Texas COGS. First, if an entity qualifies as a lending institution, that taxable entity may elect to use as COGS an amount equal to its interest expense (TX Tax Code §171.1012 (k)). Certain rental companies are also entitled to the Texas COGS deduction: motor vehicle renting or leasing companies that remit a tax on gross receipts imposed under Texas Tax Code §152.026; heavy construction equipment rental or leasing companies; or railcar rolling stock rental or leasing companies (TX Tax Code §171.1012 (k-1)).

Can a transportation company report receipts in Texas?

A taxpayer qualifying as a transportation company can report its Texas receipts based on the revenue derived from the transportation of goods or passengers in intrastate commerce within Texas or on the multiplication of total transportation receipts by total mileage in the transportation of goods and passengers that move in the intrastate commerce within Texas divided by total mileage everywhere.

Is freight forwarding a service in Texas?

The Comptroller noted that although the taxpayer may be responsible for ensuring that the goods are transported, it does not actually transport the goods, which is the responsibility of the carrier. Therefore, the receipts attributable to freight forwarding services are apportioned based on where the service is performed. This holding was followed in Letter Ruling STAR Accession No. 9510L1394D04 (October 27, 1995). In the Letter Ruling the Tax Policy Division ruled that the arranging for the shipment of freight by the freight forwarding division is the performance of a service, and the receipts attributable to freight forwarding services are apportioned based on where the service is performed. It was concluded that if the arranging is done in Texas, the receipts are treated as Texas receipts for apportionment purposes.

What percentage of revenue does a health care provider exclude from its total revenue?

A health care provider that is a health care institution shall exclude from its total revenue 50 percent of the amounts described by Subsection (n).

How much is a pro bono case in Texas?

$500 per pro bono services case handled by the attorney, but only if the attorney maintains records of the pro bono services for auditing purposes in accordance with the manner in which those services are reported to the State Bar of Texas.

What is a taxable entity that is registered as a motor carrier?

A taxable entity that is registered as a motor carrier under Chapter 643 (Motor Carrier Registration), Transportation Code, shall exclude from its total revenue, to the extent included under Subsection (c) (1) (A), (c) (2) (A), or (c) (3), flow-through revenue derived from taxes and fees.

What is a taxable entity primarily engaged in the business of providing services as an agricultural aircraft operation?

A taxable entity primarily engaged in the business of providing services as an agricultural aircraft operation, as defined by 14 C.F.R. Section 137.3, shall exclude from its total revenue the cost of labor, equipment, fuel, and materials used in providing those services.

What is a taxable entity that is primarily engaged in the business of transporting goods by waterways?

A taxable entity primarily engaged in the business of transporting goods by waterways that does not subtract cost of goods sold in computing its taxable margin shall exclude from its total revenue direct costs of providing transportation services by intrastate or interstate waterways to the same extent that a taxable enti ty that sells in the ordinary course of business real or tangible personal property would be authorized by Section 171.1012 (Determination of Cost of Goods Sold) to subtract those costs as costs of goods sold in computing its taxable margin, notwithstanding Section 171.1012 (Determination of Cost of Goods Sold) (e) (3).

What is aggregates taxable?

A taxable entity that is primarily engaged in the business of transporting aggregates shall exclude from its total revenue, to the extent included under Subsection (c) (1) (A), (c) (2) (A), or (c) (3) , subcontracting payments made by the taxable enti ty to independent contractors for the performance of delivery services on behalf of the taxable entity. In this subsection, “aggregates” means any commonly recognized construction material removed or extracted from the earth, including dimension stone, crushed and broken limestone, crushed and broken granite, other crushed and broken stone, construction sand and gravel, industrial sand, dirt, soil, cementitious material, and caliche.

What is a taxable entity that is a lending institution?

A taxable entity that is a lending institution shall exclude from its total revenue, to the extent included under Subsection (c) (1) (A), (c) (2) (A), or (c) (3), proceeds from the principal repayment of loans.

When do you have to file a franchise tax return in Texas?

As of January 1st 2020, out-of-state taxable entities with annual gross receipts over $500,000 from business in Texas must file a Franchise Tax Report even if the entity has no physical presence in this state.

When do franchises file taxes?

While the filing date for Annual Franchise Tax Reports is May 15th (in non-pandemic years), what you do the other 364 days of the year can play a big part in making sure your company pays only the minimum tax required.

How long can you carry forward a certified historic structure?

The credit can be carried forward for up to 5 years.

Why do we need to work with a tax professional?

Working with a tax professional to plan the best approach (and therefore knowing exactly what to track throughout the year) can also help avoid some of the other common mistakes we’ve seen, such as:

Does Texas have franchise tax?

Service industries, especially those with a low employee count, are generally the most affected by the Texas franchise tax as they do not have a COGS deduction. Manufacturing and retail, on the other hand, do have the COGS deduction as well as the advantage of a reduced 0.375% tax rate, both of which help minimize their tax burden.

Is a sole proprietorship taxable in Texas?

Exceptions include sole proprietorships not registered as an LLC, passive partnerships, and certain non-profits and trusts.

Does Texas have a corporate tax?

Texas is one of only six states that do not have a corporate income tax. Texas businesses are instead required to pay a franchise tax – companies pay what is basically an annual fee to Texas for the privilege of doing business in the state. It is a tax on revenue and is less than 1%.

What is franchise tax?

TAX IMPOSED. (a) A franchise tax is imposed on each taxable entity that does business in this state or that is chartered or organized in this state. (b) The tax imposed under this chapter extends to the limits of the United States Constitution and the federal law adopted under the United States Constitution.

What is a taxable entity?

DEFINITION OF TAXABLE ENTITY. (a) Except as otherwise provided by this section, "taxable entity" means a partnership, limited liability partnership, corporation, banking corporation, savings and loan association, limited liability company, business trust, professional association, business association, joint venture, joint stock company, holding company, or other legal entity. The term includes a combined group. A joint venture does not include joint operating or co-ownership arrangements meeting the requirements of Treasury Regulation Section 1.761-2 (a) (3) that elect out of federal partnership treatment as provided by Section 761 (a), Internal Revenue Code.

How long does it take to forfeit corporate privileges?

The comptroller shall forfeit the corporate privileges of a corporation on which the franchise tax is imposed if the corporation: (1) does not file, in accordance with this chapter and within 45 days after the date notice of forfeiture is mailed, a report required by this chapter;

Is a nonprofit corporation exempt from franchise tax?

A nonprofit corporation organized solely to promote the public interest of a county, city, town, or another area in the state is exempted from the franchise tax. Acts 1981, 67th Leg., p. 1694, ch. 389, Sec. 1, eff. Jan. 1, 1982. Sec. 171.058.

Is sludge exempt from franchise tax?

A corporation engaged solely in the business of recycling sludge, as defined by Section 361.003, Solid Waste Disposal Act (Chapter 361, Health and Safety Code), is exempted from the franchise tax. Added by Acts 1989, 71st Leg., ch. 641, Sec. 3, eff. Sept. 1, 1991.

Is a cooperative credit association exempt from franchise tax?

Section 2071, or an agricultural credit association regulated by the Farm Credit Administration is exempted from the franchise tax.

Is an open end investment company exempt from franchise tax?

Section 80a-1 et seq.), that is subject to that Act and that is registered under The Securities Act (Title 12, Government Code) is exempted from the franchise tax.