Exclusions tend to be based on industry, such as medical, legal, staff leasing services, and management companies (TX Tax Code §171.1011). Other exclusions include bad debt, income attributable to a disregarded entity, and net distributive income from partnerships and flowthrough partnerships (TX Tax Code §171.1011 (c) (1) (B)).

Full Answer

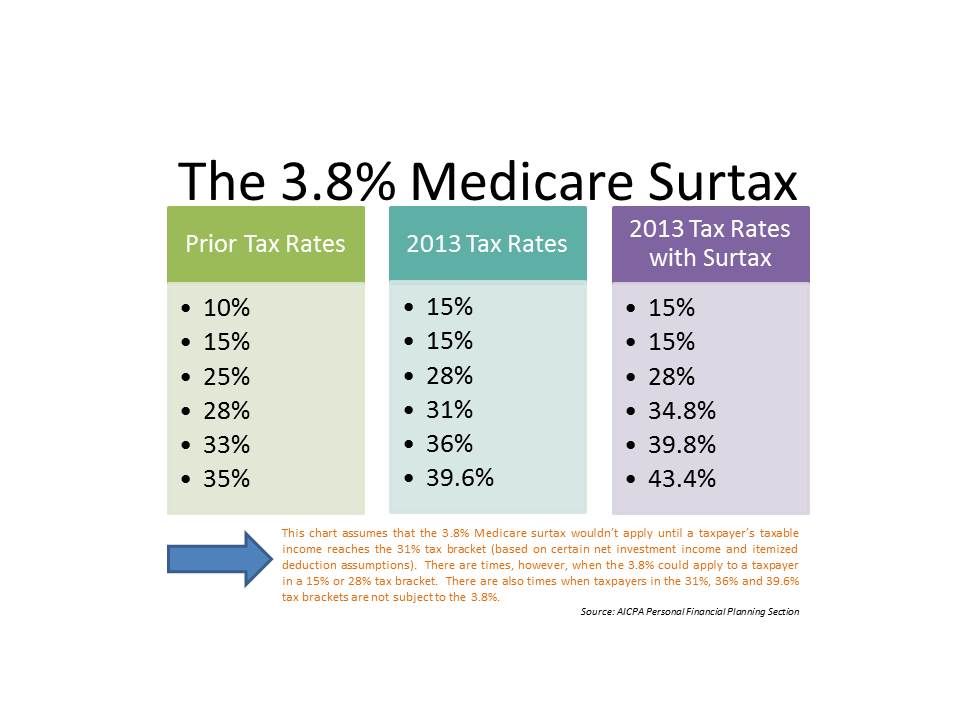

Is there a Medicare surtax on your paycheck?

Like the initial Medicare tax, the surtax is withheld from an employee’s paycheck or paid with self-employment taxes. However, there is no employer-paid portion of the additional Medicare tax, meaning the employee is responsible for paying the full 0.9%. 9

Do you have to pay taxes on Medicare benefits?

An individual’s Medicare wages are subject to Medicare tax. This generally includes earned income such as wages, tips, vacation allowances, bonuses, commissions, and other taxable benefits up to $200,000 as of 2022. 8

What is the tax rate for a franchisee?

RATES; COMPUTATION OF TAX. (a) Subject to Sections 171.003 and 171.1016 and except as provided by Subsection (b), the rate of the franchise tax is 0.75 percent of taxable margin.

Which entities are not subject to franchise tax?

Entities Not Subject to Franchise Tax. The following entities do not file or pay franchise tax: sole proprietorships (except for single member LLCs); general partnerships when direct ownership is composed entirely of natural persons (except for limited liability partnerships);

Is bad debt expensed for federal income tax purposes?

Bad debt expensed for federal income tax purposes that corresponds to items of gross receipts included in total revenue for the current reporting period or a past reporting period may be excluded from total revenue. The principal repayment of a loan is not included in total revenue and therefore cannot be excluded from total revenue as a bad debt.

Is franchise expense reimbursement included in total revenue?

Therefore, for franchise tax reporting purposes, the expense reimbursements are included in total revenue.

Can uncompensated care be subtracted from total revenue?

Yes, the costs of uncompensated care that have been excluded from total revenue may not be subtracted as cost of goods sold or compensation. If a health care provider excludes from total revenue payments received under the Medicaid, Medicare and other programs specified in Texas Tax Code (TTC) §171.1011 ...

Can a taxable entity exclude from total revenue?

Under TTC 171.1011 (e) a taxable entity can only exclude from total revenue the taxable entity's share of net income of the passive entity if the margin of a taxable entity generated the net income of the passive entity. Therefore, a taxable entity that owns an interest in a passive entity may only exclude from total revenue, to the extent included:

How is Medicare financed?

1-800-557-6059 | TTY 711, 24/7. Medicare is financed through two trust fund accounts held by the United States Treasury: Hospital Insurance Trust Fund. Supplementary Insurance Trust Fund. The funds in these trusts can only be used for Medicare.

How much Medicare tax do self employed pay?

Medicare taxes for the self-employed. Even if you are self-employed, the 2.9% Medicare tax applies. Typically, people who are self-employed pay a self-employment tax of 15.3% total – which includes the 2.9% Medicare tax – on the first $142,800 of net income in 2021. 2. The self-employed tax consists of two parts:

How Much Is the Medicare Tax Rate in 2021?

The 2021 Medicare tax rate is 2.9%. You’re typically responsible for paying half of this amount (1.45%), and your employer is responsible for the other half. Learn more.

What is Medicare Part A?

Medicare Part A premiums from people who are not eligible for premium-free Part A. The Hospital Insurance Trust Fund pays for Medicare Part A benefits and Medicare Program administration costs. It also pays for Medicare administration costs and fighting Medicare fraud and abuse.

What are the taxes that are withheld from paychecks?

Together, these two income taxes are known as the Federal Insurance Contributions Act (FICA) tax.

How many parts are there in self employed tax?

The self-employed tax consists of two parts:

Who can help with Medicare enrollment?

If you’d like more information about Medicare, including your Medicare enrollment options, a licensed insurance agent can help.

What is franchise tax?

Franchise tax is based on a taxable entity’s margin. Unless a taxable entity qualifies and chooses to file using the EZ computation, the tax base is the taxable entity’s margin and is computed in one of the following ways:

When are franchise tax reports due?

Franchise tax reports are due on May 15 each year. If May 15 falls on a Saturday, Sunday or legal holiday, the next business day becomes the due date. The Comptroller’s office will tentatively grant an extension of time to file a franchise tax report upon timely receipt of the appropriate form.

How much is the penalty for filing franchise tax return?

You can file your franchise tax report, or request an extension of time to file, online. There is a $50 penalty for a franchise tax report filed after the due date, even if no tax is due with that report and even if the taxpayer subsequently files the report.

What are the benefits provided to all personnel to the extent deductible for federal income tax purposes?

benefits provided to all personnel to the extent deductible for federal income tax purposes, including workers’ compensation, health care and retirement benefits.

Who must file a combined group report?

Taxable entities that are part of an affiliated group engaged in a unitary business must file a combined group report. Members of a combined group must use the same method to compute margin.

Do you have to file franchise tax in Texas?

Each taxable entity formed in Texas or doing business in Texas must file and pay franchise tax. These entities include:

What is franchise tax?

TAX IMPOSED. (a) A franchise tax is imposed on each taxable entity that does business in this state or that is chartered or organized in this state. (b) The tax imposed under this chapter extends to the limits of the United States Constitution and the federal law adopted under the United States Constitution.

What is an affiliated group?

In this chapter: (1) "Affiliated group" means a group of one or more entities in which a controlling interest is owned by a common owner or owners, either corporate or noncorporate, or by one or more of the member entities.

What is a taxable entity?

DEFINITION OF TAXABLE ENTITY. (a) Except as otherwise provided by this section, "taxable entity" means a partnership, limited liability partnership, corporation, banking corporation, savings and loan association, limited liability company, business trust, professional association, business association, joint venture, joint stock company, holding company, or other legal entity. The term includes a combined group. A joint venture does not include joint operating or co-ownership arrangements meeting the requirements of Treasury Regulation Section 1.761-2 (a) (3) that elect out of federal partnership treatment as provided by Section 761 (a), Internal Revenue Code.

Is a nonprofit corporation exempt from franchise tax?

A nonprofit corporation organized solely to promote the public interest of a county, city, town, or another area in the state is exempted from the franchise tax. Acts 1981, 67th Leg., p. 1694, ch. 389, Sec. 1, eff. Jan. 1, 1982. Sec. 171.058.

Is sludge exempt from franchise tax?

A corporation engaged solely in the business of recycling sludge, as defined by Section 361.003, Solid Waste Disposal Act (Chapter 361, Health and Safety Code), is exempted from the franchise tax. Added by Acts 1989, 71st Leg., ch. 641, Sec. 3, eff. Sept. 1, 1991.

Is a cooperative credit association exempt from franchise tax?

Section 2071, or an agricultural credit association regulated by the Farm Credit Administration is exempted from the franchise tax.

Is an open end investment company exempt from franchise tax?

Section 80a-1 et seq.), that is subject to that Act and that is registered under The Securities Act (Title 12, Government Code) is exempted from the franchise tax.

What is the exemption for franchise tax in Texas?

One of the most important exemptions for the Texas franchise tax is the exempt passive entity. Exempt passive entities will be required to file annual information statements to verify that the passive entity qualifications are met, but they will owe zero tax.

When are franchise taxes due?

Due to the late release of the forms and the complexity of the tax, the comptroller’s office extended the due date of the franchise tax for both initial and annual filers from May 15 to June 16. The tax is still technically due on May 15, but the penalty is waived for this one-month period.

What is a taxable entity in Texas?

In addition, taxable entities include not only corporations and LLCs, but generally any entity with limited liability protection. Also introduced for the first time in Texas is the idea of unitary filing, something very alien to Texans. The only things that did not change are the due date of the tax, May 15 of each year, and the tax’s accounting period rules.

How is total revenue determined in Texas?

Total revenue is determined by extracting revenue from specific lines on the federal income tax forms (TX Tax Code §171.1011 (c) (1) (A)). Next, total revenue is reduced by applicable exclusions per Texas law. Exclusions tend to be based on industry, such as medical, legal, staff leasing services, and management companies (TX Tax Code §171.1011). Other exclusions include bad debt, income attributable to a disregarded entity, and net distributive income from partnerships and flowthrough partnerships (TX Tax Code §171.1011 (c) (1) (B)).

Is there a tax due on $300,000?

No tax is due if the total revenue after revenue exclusions is less than $300,000 (TX Tax Code §171.002 (d)). Due to the interaction between the small business discount and the E-Z computation, a taxable entity will owe zero tax with reportable revenue of $434,782 or less.

Can passthrough income be excluded from total revenue?

Note that for net distributive income (i.e., passthrough income) to be excluded, it must be from a taxable entity treated as a partnership or an S corporation for federal income tax purposes. Passthrough income from an exempt entity (including passive entities) generally cannot be excluded from total revenue. The reason for this special exclusion is to prevent double taxation.

Is intercompany revenue excluded from total revenue?

Intercompany revenue from affiliated entities is excluded from total revenue if the entities are part of a filing unitary group (TX Tax Code §171.1014 (c)). Note that a corresponding deduction may need to be made in the cost of goods sold (COGS) deduction or compensation deduction if the revenue is directly related to those costs.

What is the purpose of exclusion in Titan Transportation v. Combs?

Combs, the Austin Third Court of Appeals held the taxpayer was entitled to exclude from total revenue payments made to its subcontractors that were providing services for its customers under Texas Tax Code (TTC) § 171.1011(g)(3), which provides: “A taxable entity shall exclude from its total revenue…only the following flow-through funds that are mandated by contract to be distributed to other entities...”2 The Third Court of Appeals explained that the term “other entities” means someone other than the taxpayer and further clarified: “[the] purpose of the (g)(3) exclusion is to prevent double taxation of funds that are not truly gain or income to the taxpayer, and this purpose is satisfied regardless of whether the mandate is contained in a contract with a customer or with a subcontractor.”3

What is the COGS deduction in Combs v. Newpark?

Newpark Resources Inc., the Third Court of Appeals found the taxpayer’s activities of removal and disposal of waste materials from oil and gas well drilling sites qualified for a COGS deduction under TTC § 171.1012(i).4 TTC § 171.1012(i) provides: “A taxable entity furnishing labor or materials to a project for the construction, improvement, remodeling, repair, or industrial maintenance of real property is considered to be an owner of that labor or materials and may include the costs…in the computation of cost of goods sold.”

What if an employer does not deduct Medicare?

An employer that does not deduct and withhold Additional Medicare Tax as required is liable for the tax unless the tax that it failed to withhold from the employee’s wages is paid by the employee. An employer is not relieved of its liability for payment of any Additional Medicare Tax required to be withheld unless it can show that the tax has been paid by filing Forms 4669 and 4670. Even if not liable for the tax, an employer that does not meet its withholding, deposit, reporting, and payment responsibilities for Additional Medicare Tax may be subject to all applicable penalties.

What is Medicare tax?

The Additional Medicare Tax applies to wages, railroad retirement (RRTA) compensation, and self-employment income over certain thresholds. Employers are responsible for withholding the tax on wages and RRTA compensation in certain circumstances.

What happens if an employee does not receive enough wages for the employer to withhold all taxes?

If the employee does not receive enough wages for the employer to withhold all the taxes that the employee owes, including Additional Medicare Tax, the employee may give the employer money to pay the rest of the taxes.

How to calculate Medicare tax?

Step 1. Calculate Additional Medicare Tax on any wages in excess of the applicable threshold for the filing status, without regard to whether any tax was withheld. Step 2. Reduce the applicable threshold for the filing status by the total amount of Medicare wages received, but not below zero.

How much did M receive in 2013?

M received $180,000 in wages through Nov. 30, 2013. On Dec. 1, 2013, M’s employer paid her a bonus of $50,000. M’s employer is required to withhold Additional Medicare Tax on $30,000 of the $50,000 bonus and may not withhold Additional Medicare Tax on the other $20,000.

How much is F liable for Medicare?

F is liable to pay Additional Medicare Tax on $50,000 of his wages ($175,000 minus the $125,000 threshold for married persons who file separate).

When is Medicare tax withheld?

An employer is required to begin withholding Additional Medicare Tax in the pay period in which it pays wages in excess of $200,000 to an employee.